RCM in 2025 and Beyond: The Next Growth Wave, Technology, and Consolidation

Revenue Cycle Management (RCM) in the New Era of Healthcare has developed into a vital financial performance driver for healthcare providers worldwide. In 2025, RCM will clearly change from being a backend cost center to a strategic, technology-driven growth facilitator. The need for scalable, automated, and analytics-driven RCM solutions is growing due to growing expenses, complicated regulations, and a persistent labor shortage. Payers and providers are reconsidering how they handle revenue flows from beginning to end, especially in the US, which makes up more than half of the worldwide market.

RCM is being redefined globally by AI-led automation, predictive analytics, and digitalized patient involvement; it is no longer just about basic claims processing. This change offers RCM firms a significant chance to grow, add unique value, and take part in the larger transformation of healthcare delivery, especially through smart M&A options.

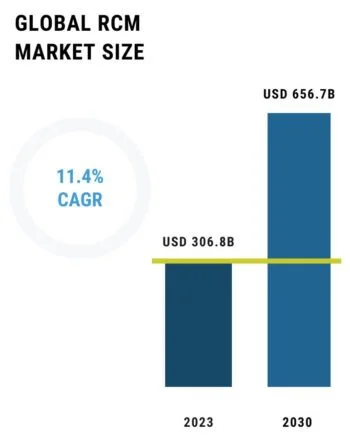

RCM Market Size and Prospects for Growth

With a strong 11.4% CAGR during the timeframe, the worldwide RCM market is expected to more than double to USD 656.7B by 2030 from USD 306.8B in 2023. At USD 155.6 billion in 2023 and expected to reach over USD 310 billion by 2030 at a rate of 0.3% CAGR, the U.S. continues to be the largest single market. This dominance is supported by its sophisticated payor environment, intricate reimbursement regulations, and early adoption of AI. Asia Pacific and Europe are becoming the fastest-growing regions, notwithstanding North America's absolute advantage, due to:

Digital Health Initiatives: Digital claims submission and interoperability are required by national e-health programs in countries such as China, Germany, and India.

Outsourcing and Offshore Hubs: As healthcare prices rise in developed economies, outsourced RCM operations are being moved to less expensive locations in Eastern Europe and Asia.

Reasons for the Growth of RCM

Growing Cost Pressures: RCM becomes a key tool for recovering lost income through quicker claims processing and rejection management as provider operating margins shrink due to growing clinical expenses.

Regulatory and Value-Based Complexity: Platforms that can automate compliance and codify results are in high demand due to the transition from fee-for-service to value-based payment models, which necessitate end-to-end integration of clinical and financial data.

Workforce Shortages & Skill Gaps: Providers outsource to technology-augmented RCM vendors that combine offshore talent pools with AI-driven automation due to persistent workforce shortages in coding and billing.

Patient-Centric Billing: Patient financial engagement is becoming a competitive differentiator due to rising customer expectations for clear, user-friendly billing portals with real-time estimations, several payment methods, and self-service features.

Data and Analytics Imperatives: With hundreds of millions of claims handled annually, RCM is evolving from a back-office cost center into a strategic analytics hub thanks to its capacity to mine patterns and forecast denials, optimize cash-flow timing, and assess performance.

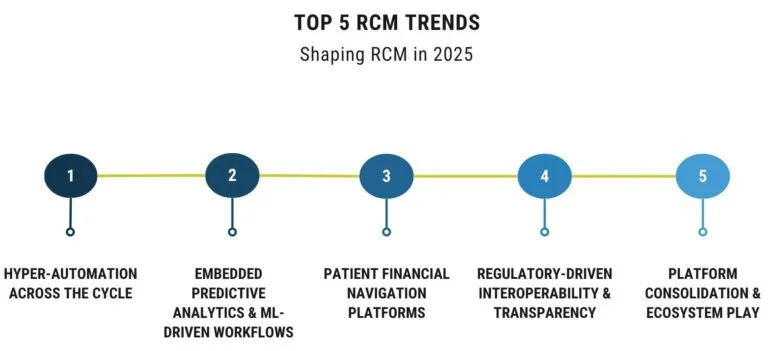

2025's Top 5 Trends Affecting RCM

Hyper-Automation Across the Cycle: By automating repetitive operations like eligibility checks and remittance reconciliation, end-to-end robotic process automation (RPA) in conjunction with generative AI frees up staff members to concentrate on exception handling and strategic collaborations.

Embedded Predictive Analytics & ML-Driven Workflows: Real-time dashboards that predict cash collection timings, denial hotspots, and days-in-AR are quickly becoming commonplace. Prominent platforms use machine learning to dynamically redistribute task queues and suggest next-best actions.

Patient Financial Navigation Platforms: In order to lower bad debt and raise satisfaction levels, integrated "financial care coordinator" modules are being developed to assist patients with cost estimates, payment schedules, and financial aid programs.

Regulatory-Driven Interoperability & Transparency: RCM systems must open APIs and effortlessly communicate data across EHRs, payors, and patient portals in order to comply with new regulations pertaining to price transparency and interoperability (such as the US No Surprises Act and EU digital health standards).

Platform Consolidation & Ecosystem Play: To increase account penetration and secure multi-year contracts, RCM suppliers are combining related services including clinical documentation enhancement, code audit, and patient interaction into one platforms.

The Wave of Consolidation

Even though the worldwide RCM industry is expected to reach over $306 billion in 2023, it is still quite fragmented, with over 75% of providers earning less than $30 million in EBITDA, leaving a wide range of mid-market companies ready for consolidation. Strategic buyers and private equity have taken notice and are investing large sums of money in high-profile transactions.

The most appealing RCM suppliers have three key characteristics in common with investors and creators hoping to spearhead or profit from this wave of consolidation:

Deeply Embedded Client Relationships: Top RCM providers negotiate multi-year agreements that usually last two to five years and have renewal rates above 95%. These agreements result in highly predictable, stable revenue streams. With recurring subscription-style fees accounting for more than 80% of their revenue, leading RCM businesses usually win annual contract renewal rates above 95%, guaranteeing highly predictable, "sticky" cash flows. Performance-based incentives, which further align provider and client goals, lower churn, and increase customer lifetime value, are currently included in approximately 70% of RCM agreements throughout the industry.

Proprietary Automation & AI Frameworks: Top-tier RCM systems use AI-powered solutions that reduce turnaround times by up to 50% and reduce human billing hours by tens of thousands every month. Up to 60–70% of document workflows are now automated by best-in-class RCM platforms, saving tens of thousands of labor hours every month, reducing end-to-end documentation cycles by about 40%, and increasing client ROIs by 25–35%. As providers adopt AI-led efficiency, the outsourced RCM market is expected to nearly double in six years, from $141.6 billion in 2024 to $272.8 billion by 2030.

Specialized Knowledge in High-Value Niches: By mastering workflow and precise coding, RCM companies that concentrate on complex specialties like radiology, anesthesia, and behavioral health can command 20–30% greater margins. Clean-claims rates in the mid-90s percentile are frequently attained by specialized RCM teams working on complicated service lines. This results in much lower denial-related rework costs and increases net collections by about 10% to 15%. This degree of specialization turns into a potent competitive differentiator given industry benchmarks of 5-8% first denial rates.

The Reasons Behind Private Equity's Interest

Dedicated healthcare funds accounted for a record 5% of all PE fundraises in 2024, or around $45 billion, a 9.3% increase over 2023, according to PitchBook's H2 2024 Healthcare Funds Report. Because lending rates have relaxed and lower valuations may encourage more mergers, this year is predicted to be a healthier year for the industry. RCM has emerged as a PE favorite due to a number of potent dynamics:

Rapid market expansion and premium margins: The RCM market in the United States alone is expected to grow at an annual pace of 10.1 percent, from $172.2 billion in 2024 to over $308 billion by 2030. Thanks to efficient, high-value procedures, top RCM experts maintain EBITDA margins in the mid-20s, which are significantly higher than the ~10.8 percent average for hospital operations.

Mission-critical, non-discretionary service: RCM is the foundation of almost every provider's cash flow; inefficient billing causes payments to be delayed and accounts receivable days to soar, endangering a hospital's operational liquidity. Because of this, RCM is always a key concern, even during recessions.

Predictable, persistent revenue streams: PE purchasers value subscription-style revenues at EV/Revenue multiples up to 6.1× in mid-market transactions when top RCM vendors obtain 3–5 year contracts with renewal rates above 90%.

Scalable margin expansion through technology and offshore leverage: AI and offshore delivery models are used to provide scalable margin expansion. While offshore operations can contribute to labor cost reductions of 25–30%, resulting in significant efficiency improvements, AI-driven claim scrubbing can lower denial rates by up to 30% and increase resubmission turnaround by up to 50%.

Plenty of dry powder and easing financing: With central banks indicating rate reduction and global PE dry powder close to $3.2 trillion, sponsors are well-positioned to invest in robust, high-visibility industries like RCM, where lower entry multiples and steady cash flows provide attractive risk-adjusted returns.

RCM is a unique opportunity for PE in 2025 because to the combination of strong growth, mission-critical economics, technology-driven leverage, and consolidation tailwinds.

Increased investor interest is indicated by recent M&A activity.

HEALTHFUSE AND INTANDEM CAPITAL

Healthfuse, a Milwaukee-based business that specializes in revenue cycle vendor management, has received investment from InTandem Capital Partners, a New York-based private equity firm with a focus on healthcare. Healthfuse uses analytics and technology to lower costs for hospitals and health systems while enhancing vendor performance. The business intends to extend its data-driven platform and scale its services with InTandem's help in order to satisfy the rising need for more effective RCM solutions.

HEALTHYBOS AND KNACK RCM

Knack RCM, a tech-enabled RCM services provider based in New Jersey, purchased HealthyBOS, a US and Philippines-based RCM company with more than 200 workers that specialized in DME billing. Through this acquisition, Knack RCM strengthens its presence in the DME RCM market and grows its staff in the Philippines, improving its fulfillment capabilities. The agreement demonstrates Knack RCM's dedication to voice-enabled, scalable services for payors and healthcare providers.

WEE HEALTHEK AND TA ASSOCIATES

A controlling interest in Vee Healthtek, a Bengaluru and US-based healthcare IT company with expertise in revenue cycle management, professional billing, and IT services, was purchased by Boston-based private equity firm TA Associates. This is TA's first large investment in the RCM industry and its second in India. The $250 million purchase intends to boost Vee Healthtek's growth through strategic acquisitions and organic expansion.

ARSENAL CAPITAL AND HEALTH KNOWLEDGE

Knowtion Health, a provider of AI-enabled revenue cycle insurance claim resolution services, was purchased by Arsenal Capital Partners. Knowtion Health, a Florida-based company, specializes in handling complicated insurance claims for hospitals and health systems. It does this by utilizing its exclusive ClaimBRAIN platform, which combines generative AI, machine learning, and natural language processing to improve efficacy and efficiency. In more than 40 US states, the company provides services to more than 500 hospitals. The present majority owner, Sunstone Partners, kept a sizeable strategic co-investment in the business.

HBCS AND MED-METRIX

Hospital Billing & Collection Service (HBCS), a Delaware-based company that specializes in patient financial involvement and insurance reimbursement services, was purchased by Med-Metrix, a US-based supplier of technology-enabled RCM solutions. By combining HBCS's experience with its own extensive service offerings, this acquisition strengthens Med-Metrix's end-to-end RCM capabilities. The united organization hopes to improve patient experiences and financial results for US healthcare providers.

What do these transactions indicate?

Three distinct themes emerge from the recent spate of deals, which range from targeted bolt-on add-ons to high-profile multibillion-dollar take-privates:

Consolidation of Dispersed Mid-Market Players: Several deals highlight private equity's need for stable, mid-market platforms with performance-based, sticky contracts.

Tech-Enabled, AI-First Platform Building: A calculated risk to provide end-to-end automation by bringing complementing AI engines together under one roof.

Geographic & Service-Line Expansion: Emphasizes the development of offshore capacity as a fundamental strategy for labor arbitrage and round-the-clock service provision.

De-Risked Growth Models: To improve revenue visibility and support premium valuations, acquirers give priority to contracts with strong renewal rates and performance incentives.

Platform-Driven Upsell: By incorporating related services (eligibility, documentation, coding audits), purchasers hope to increase their market share and forge stronger barriers to entry.

Global Delivery Networks: Strategic agreements are not limited to the United States. scale; in order to control labor costs and provide seamless service to multinational clients, they are building worldwide delivery networks.

When taken as a whole, these transactions show that the market is at a turning point, moving from dispersed, service-only suppliers to integrated, technology-driven platforms designed for long-term growth, resilience, and scale.

Prospects for 2025 and Later

In 2025, RCM will be a tactical tool. RCM companies have a once-in-a-decade chance to scale, specialize, and redefine value delivery due to the convergence of consumer expectations, automation, payer change, and regulatory obligations. Now is the moment for creators and operators to assess whether investment, organic development, or strategic alignment could lead to the next stage of wealth generation. Financial and strategic investors are genuinely interested and are becoming more so.

Through improved access to cash, technological investments, and better service capabilities, M&A opportunities provide acquisition targets improved growth prospects. These businesses may scale operations, expedite innovation, especially in automation and artificial intelligence, and increase their clientele by collaborating with larger platforms and seasoned investors. Furthermore, integration into consolidated organizations enhances competitive distinctiveness, operational efficiency, and market positioning, allowing objectives to better meet changing industry demands and gain a larger market share.

As a result, we anticipate that over the next ten years, the most prosperous RCM businesses will be those that combine in-depth market knowledge, exclusive automation technologies, and scalable operations while actively seizing new opportunities.

Leading global investment banking firm GTD, which specializes in strategic investments and M&A transactions in the Technology, Media, and Telecom (TMT) sectors, is at the forefront of helping businesses realize the transformative potential of Generative AI. GTD's expertise in growth capital, M&A transactions, and strategic investments enables investors and entrepreneurs to maximize AI adoption, scale innovation, and promote sustainable growth. Success in the quickly changing AI landscape depends on forming strategic alliances that enable businesses to take the lead in the upcoming wave of digital transformation by unlocking efficiency, scalability, and competitive advantage.