Sector Analysis: 2023 Cloud Technologies M&A

The demand for more effective and secure managed IT and cloud solutions has increased due to remote and hybrid work environments. The requirement for highly specialized skills in cyber security and digital and cloud transformation grew as the adoption of a digital-first work paradigm advanced. Siemens' $1.88 billion acquisition of Brightly Software led the $2.9 billion in cloud M&A transactions in the North American technology sector in June 2022, according to GlobalData's deals database. In Q1 2022, global spending on cloud infrastructure services amounted to $55.9 billion, a 34% increase over Q1 2021. When comparing Q1 2022 to Q1 2021, the Big Three CSPs—AWS, Azure, and Google Cloud—grew at a combined rate of 42%.

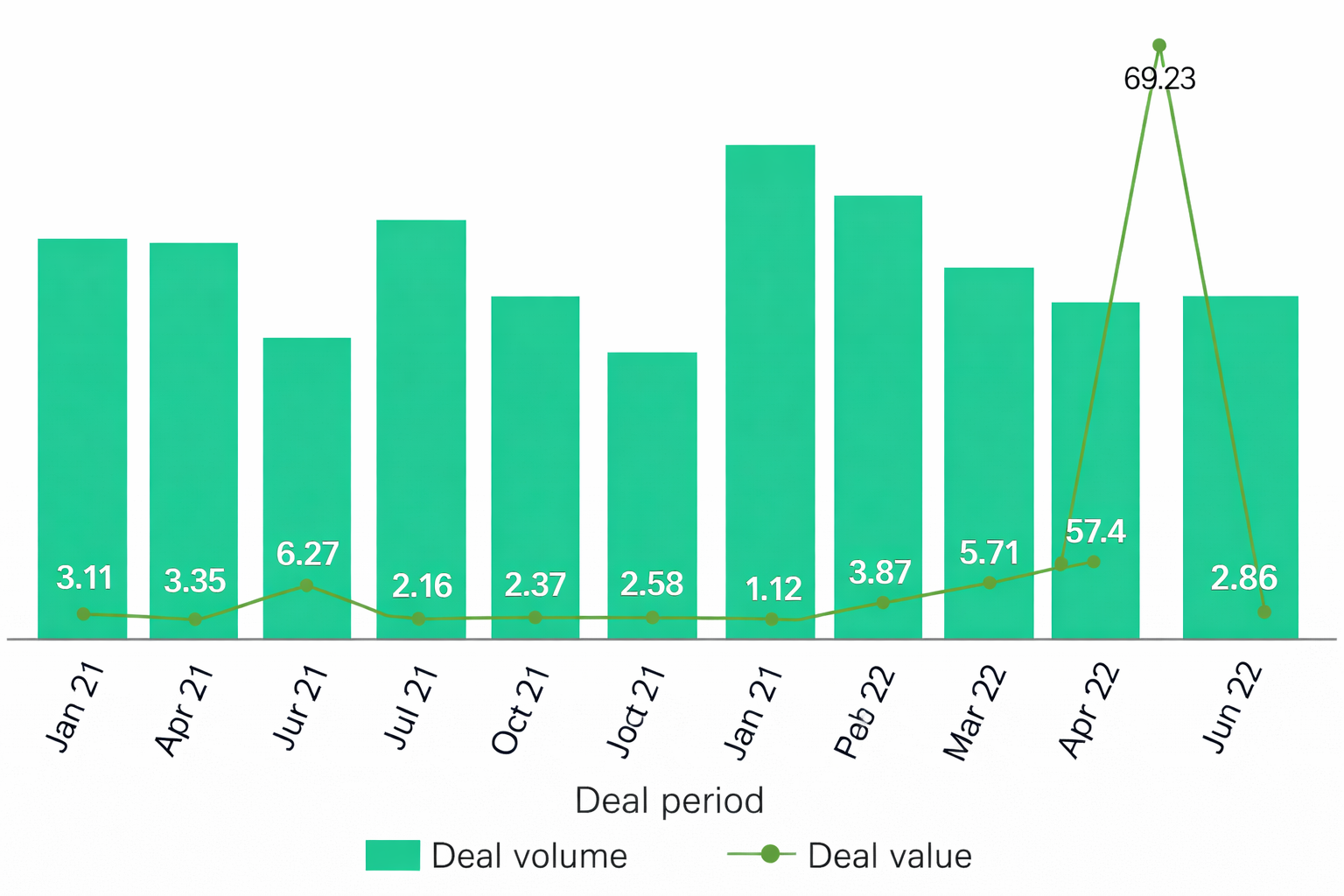

Cloud M&A transactions in the technology sector in North America: Value and volume trend from June 2021 to June 2022

The deal value has decreased by 69.2% when compared to the $9.29 billion 12-month average. On the other hand, the April–June quarter was unstable.

In June 2022, North America accounted for 75.66% of the $3.78 billion worldwide technology industry cloud M&A deal value. The US led North America in cloud M&A deal value throughout the technology sector, with a 75.66% share and agreements valued at $2.86 billion.

In terms of cloud M&A deal activity, North America saw 42 deals in June 2022, up 10.53% from the previous month and down 4.55% from the 12-month typical. 36 agreements were made in the US during the month.

In Q4 2022, global spending on cloud infrastructure services increased by US$12.3 billion, or 23%, to reach US$65.8 billion. From US$191.7 billion in 2021 to US$247.1 billion in 2022, the total amount spent on cloud infrastructure services increased by 29%. In comparison to Q1 2022, the quarterly growth rate decreased by more than 10 percentage points (34% in Q1 2022 versus 23% in Q4 2022). However, Canalys predicts that spending on worldwide cloud infrastructure services will rise by 23% for the entire year in 2023 as opposed to 29% in 2022.

The $13.8 billion leveraged acquisition of Citrix Systems by TIBCO in January increased M&A activity to $104.7 billion this year. The $61.0 billion purchase of VMware by Broadcom in May was one of the other big transactions.

Motivators behind Cloud M&A

Cloud migration has driven huge IT companies to hasten new product deployments at a time when many younger, smaller enterprise IT companies are winning via innovation and speed of execution. The complexity and cost of new IT systems, cloud technologies, and modifications to legacy systems are all rising. In complicated cloud settings, organizations require assistance with infrastructure, scaling, and security management. Large enterprises like using specialized ITSM services to better handle the cost, security, and infrastructure challenges that CIOs are facing. According to Forrester's 2022 Infrastructure Cloud Survey, 40% of businesses will implement a cloud-native-first approach in 2023 to increase agility, efficiency, and cost. In order to close technological gaps, gain market share, pursue roll-up plans, and acquire talent, they are looking for specialist cloud and managed service providers. This has resulted in a notable surge in acquisitions in 2022.

Drivers of Cloud Expertise Demand

Highlighted 2022 and 2023 Transactions

Itoc purchases ThoughtWorks

With more than 12,000 workers and AWS Premier Tier Services Partner status in 2022, Chicago-based ThoughtWorks is an expert in Agile development (Scrum, XP, Lean), retail customer experience consulting, management consulting, data science and analytics, product innovation, open source communities, continuous delivery, user experience design, Agile development tools, and mobile strategy.

Cloud computing, DevOps, AWS consulting, cloud architecture, managed AWS, proof of concepts, cloud cost optimization, training & community, cloud engineering, open source, managed services, cloud applications, eCommerce, cloud enablement, business transformation, SaaS, AWS, and IntelligentOps are among the areas of expertise for Queensland, Australia-based Itoc, which was established in 2012.

Thoughtworks' cloud service line, platforms, and enterprise modernization in Australia are all improved by the Itoc acquisition. Combining the forward-thinking work cultures, values, and innovative spirit of Itoc and Thoughtworks will let their clients use their IT infrastructure on a flexible AWS cloud platform to innovate and run their businesses more creatively and efficiently.

Centrilogic acquires WatServ

With more than 200 employees, Centrilogic is a Mississauga-based company that specializes in Agile and DevOps, application management, managed cloud, public, private, multi-cloud, hybrid cloud, cloud security, Microsoft Azure, AWS, OCI, co-location, data centers, disaster recovery, private networking, SD-WAN, cloud connectivity, databases, advanced applications, digital transformation, IT transformation, and digital touchpoints.

WatServe, a Toronto-based company with more than 70 employees, specializes in IT consulting, infrastructure modernization, cloud-managed services, cloud assessment, cloud migration, hybrid, public, multi-cloud, cybersecurity, security operations center-as-a-service (SOCaaS), disaster recovery, Microsoft Azure, Azure Virtual Desktop, modern workplace, M365, desktop-as-a-service, network management, migration of SQL Server to Azure, managed Microsoft Dynamics (AX, GP, NAV, 365BC), Google Cloud Platform, Amazon AWS, and WatServe has several Azure Advanced Specializations and Solution Partner Designations.

Centrilogic can boost its strategic advising, cloud, cybersecurity, and application management services while accelerating its expansion strategy by utilizing WatServ's cloud expertise. This will allow Centrilogic to increase its footprint in both Canada and the US. From strategic advice and consultation to deployment and continuous optimization, they will use WatServe to design and deliver a suitable end-to-end solution.

WatServ's vision and culture are comparable. Clients will gain from utilizing Centrilogic's DevOps, cloud-native application development and management, and data and analytics skills, which will enable them to innovate and gain a competitive edge as well as measurable commercial success.

Pandera Systems and Google Cloud Partners 66degrees combine.

With additional funding from Sunstone Partners, a growth equity-focused private equity firm, 66degrees, a Google Cloud Premier Partner, announced its merger with Pandera Systems. Sunstone Partners increased its investment in 66degrees and Pandera, two distinctive businesses that came together to form the second-largest pure-play Google Cloud services leader in North America in terms of professional services revenue and personnel count. Google Cloud, cloud adoption, security, cost optimization, cloud-native application development, data modernization, app modernization, and cloud engineering are among the areas of expertise for Chicago-based 66degrees, which employs more than 350 people.

Business intelligence, analytical applications, predictive analytics, business process transformation, alliance and managed services, data science, cloud services, Google Cloud, enterprise decision automation, systems integration, information management, and product innovation are among the areas of expertise for Orlando-based Pandera Systems.

With 500 workers and more than 375 GCP and GWS certifications, the merged business will provide a wider range of Google Workspace solutions, DevOps transformations, cloud-native application development, modernization of Google Cloud data and analytics, and cloud infrastructure. With substantial complementarity and synergies, the merger brings together two of the most cutting-edge Google Cloud services companies in the world, enabling them to provide clients with top-notch cloud migration, infrastructure, security, application modernization, and enterprise productivity solutions.

Toward the future

In many respects, the use of cloud computing kept growing until 2022. Due to the uncertain macroeconomic climate, many organizations made more plans and investments than they had in the past in developing unique cloud capabilities and their future growth strategy. For cloud organizations that make proactive investments to safeguard future growth and are well-positioned to unleash significant value, most of this planning should pay off in 2023 and beyond. For example, according to Gartner, expenditures in cloud applications would climb by 11.3% to $879.62 billion in 2023, driving a 5.1% increase in worldwide IT spending to $4.6 trillion.

At GTD, we think that the markets for cloud experts and MSPs are still very fragmented, which should present a lot of chances for private equity and strategic investors to help specialized Cloud companies get "founder-friendly" growth capital and generate win-win situations for long-term expansion or mergers and acquisitions.

Looking more closely at the cloud MSP market, more businesses are getting ready to deploy better internal solutions to increase productivity and scale. These include self-service apps to assist customers in resolving issues with identified chatbots, push notifications, and time management, among other things. As cloud use increases, MSPs will use automation and remote teams in place of on-site staff, enabling them to grow from regional to national and, for larger MSPs, international markets. GTD predicts that as Cloud MSPs seek to boost revenue growth and spur higher levels of innovation in their capabilities and offers, flexible loan or equity-based investment opportunities will significantly increase through 2023 and beyond.